The Vietnamese version is available here.

Click here to download the PDF version.

On August 1, 2024, the three most pivotal legal documents within Vietnam’s real estate legal framework, namely the Land Law 2024, the Real Estate Business Law (“REB Law“) 2023, and the Housing Law 2023, came into effect. Together with certain related provisions in the Credit Institutions Law 2024, these laws are set to significantly impact the real estate market in Vietnam.

Vilasia, in collaboration with The Saigon Times, is pleased to present a series of analytical articles by Vilasia’s Nhung Nguyen on the most noteworthy new regulations in these four legal documents. The series will focus on six main topics:

(i) Methods for determining land rent and land use fees;

(ii) Conditions and procedures for transferring real estate projects;

(iii) Specific regulations on commercial housing projects;

(iv) Specific regulations on industrial park projects;

(v) Implementation of projects in the form of subdividing land lots for sale; and

(vi) Expansion of business scope for enterprises with foreign investment.

Below is the third in the series entitled “Specific regulations on commercial housing projects”, originally published in Vietnamese in The Saigon Times on August 8, 2024. The digital version is available here.

____________________________

Investors will have to find their own land fund for commercial housing project development

This policy is clearly affirmed in Article 127 of the Land Law 2024, where commercial housing projects can be implemented via: (i) agreements on receiving land use rights with landowners; or (ii) using the investor’s own existing land to implement projects if they meet the legal conditions. Thus, the State shalll not acquire land to implement commercial housing projects.

Also related to commercial housing development, in cases where the commercial housing development area is within the scope of an urban area project, instead of the State acquiring land to develop all urban area projects as in the Land Law 2013, from now on, only urban area projects that fully meet the following conditions will have the State acquire land and allocate/lease it to investors:

- Have mixed-use functions;

- Have synchronized technical infrastructure and social infrastructure systems with housing as prescribed by construction laws to build new or renovate and improve urban areas.

The limitation of cases where the State acquires land aims to reduce the large volume of site clearance work for state agencies, while potentially accelerating the compensation and site clearance step due to greater flexibility when investors negotiate more equally with landowners. Therefore, the Land Law 2024 provides many policies to encourage investors to negotiate to receive land use rights, such as allowing landowners to not need a Land Use Right Certificate if they already meet the conditions for issuance, while allowing the skipping of the land use term extension procedure when expired if the investor has received land use rights but has not completed the administrative procedures to record this transaction.

However, from the investors’ perspective, limiting the type of land for commercial housing development will cause many difficulties and shortcomings. Specifically, it must be residential land if the investor agrees to receive land use rights from landowners; and must be residential land or residential land and other land if the investor already has land use rights. Thus, if the land area does not contain any residential land area despite being consistent with land use planning, investors who already have land use rights will not be able to propose commercial housing projects. Especially, in cases of negotiating to receive land use rights for commercial housing development, investors will not be able to implement if there is any land area other than residential land in the project land area.

To address this shortcoming, as soon as the Land Law 2024 was approved, the Government directed relevant ministries and agencies to develop a pilot project for the Government to submit to the National Assembly for consideration and issuance of a Resolution allowing pilot implementation of commercial housing projects through agreements on receiving land use rights or having land use rights for land other than as stipulated by law.

Particularly for foreign investors, this regulation will limit to the extent that foreign investors seemingly cannot have land use rights to implement commercial housing projects when foreign investors cannot receive land use rights from other land users (except for land in industrial parks, industrial clusters, high-tech zones)[1]. Meanwhile, the State will not acquire land to allocate to foreign investors to implement commercial housing projects in any case. This may leave foreign investors with only the option of acquiring existing commercial housing projects.

Limiting deposit amounts and the timing of collecting deposits for future real estate purchases

This is a very new regulation in the REB Law 2023, limiting deposits to no more than 5% of the selling price or lease-purchase price of houses, construction works, or floor area in construction works. At the same time, the timing for collecting deposits is only when the houses or construction works have met all conditions to be put into business as stipulated by the REB Law 2023[2].

With this new regulation, it’s clear to see the State’s effort in maximally protecting the rights of buyers of future real estate – the weaker party in this purchase relationship – against the situation where investors mobilize large amounts of money from home buyers in the form of deposits from very early stages of the project but delay construction and completion for handover to home buyers. Previously, deposits for future real estate purchases were implemented according to the Civil Code provisions, which had no restrictions on the amount or timing of deposits.

However, this regulation is considered too strict for investors of future real estate projects, as the typical deposit amount for real estate transactions is 10-20% instead of 5% as stipulated by law. Regarding the timing of receiving deposits, which is from when the houses or construction works have met all conditions to be put into business, meaning when the investor has all the documents to open sales of future real estate. At this point, the investor already has all the documents on land use rights, has completed financial obligations on land, and has implemented construction and completed technical infrastructure and foundations (for apartments and mixed-use buildings), meaning the investor has gone through almost difficult stages in terms of administrative procedures as well as financial arrangements for the project. And with this condition, the investor and the buyer are allowed to sign a contract for the sale of future real estate without the need to sign a deposit agreement. Thus, it can be seen that the deposit has no significant meaning for the investor, and conversely, buyers who want to make early deposits to enjoy more incentives and priorities from the investor will also find it difficult to achieve their goals.

Issuance of bank guarantees is no longer a mandatory obligation for investors

Specifically, bank guarantees for the financial obligations of investors when not delivering houses as committed will be chosen by the buyer or lease-purchaser[3]. In cases where the buyer or lease-purchaser chooses not to require this guarantee, the investor will be able to skip a procedural step when implementing the future real estate purchase contract. This will help save the cost of issuing bank guarantees – a type of cost that will be included in the transfer price of future real estate, which ultimately benefits the buyer or lease-purchaser. However, in practice, with contracts signed according to templates issued by investors and the unbalanced position of buyers or lease-purchasers compared to investors, this right of choice for buyers or lease-purchasers may not be implemented in the spirit of the law.

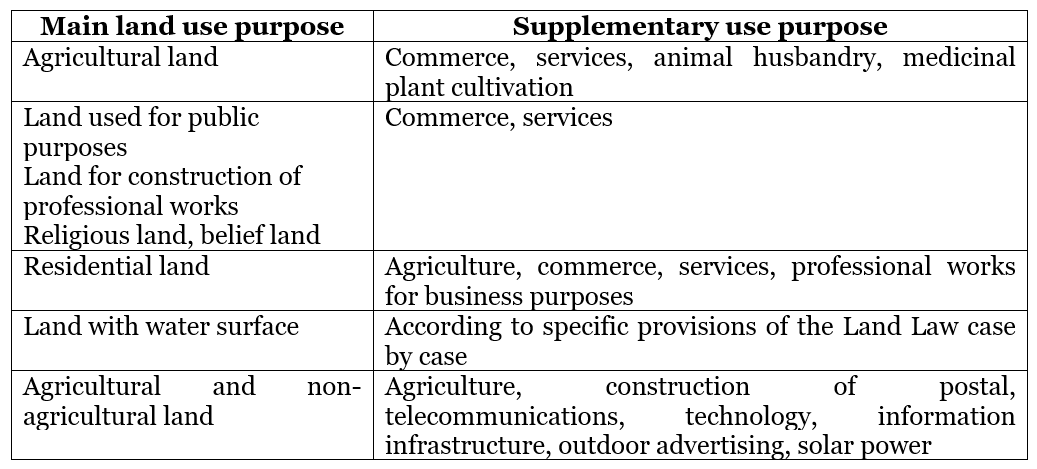

The Land Law 2024 expands the rights of land users in the form of multi-purpose combined use, specifically as follows[4]:

Specifically for housing, the Housing Law 2023 adds similar provisions on the permission to build and use in combination with other purposes, along with stricter requirements and conditions to ensure the main purpose of housing use[5]. Specifically, lawmakers require clear determination of the use purpose at the step of applying for project approval; issues related to the design and construction of functional areas to ensure operation; and require synchronized technical and social infrastructure within and outside the project scope.

One of the real estate products directly benefiting from this open policy is Condotel (tourist apartments), Officetel (office apartments), etc. The development of these real estate products currently faces obstacles in issuing Land Use Right Certificates for a long time, recently resolved by Decree 10/2023/ND-CP regulating the issuance of certificates for construction works used for tourist accommodation purposes according to tourism law regulations on commercial and service land, and Official Letter 3382/BTNMT-DD of the Ministry of Natural Resources and Environment dated May 15, 2023, on issuing certificates for two cases: construction works on non-agricultural land that is not residential land (with a time limit); and mixed-use apartment buildings built on residential land, where part is used for mixed purposes (long-term). However, the Land Law 2024 and Housing Law 2023 only address the situation of Condotels and Officetels on residential land and have not provided guidance for cases built on other land types, while these products are mainly developed on commercial and service land.

Nevertheless, with this newly added regulation along with conditions and requirements considered very detailed and specific, the use of land and structures on land will become more flexible and diverse, contributing significantly to increasing land use efficiency in the context of very diverse actual land use needs while still ensuring construction order, fire prevention and fighting, environment, and security and social order.

[1] Article 28.1, Land Law 2024

[2] Article 23.5, REB Law 2023

[3] Article 26 REB Law 2023

[4] Article 218 Land Law 2024

[5] Article 33 Housing Law 2023

Download the PDF version of this article here.